When using the cash accounting scheme and part of a growing business, it is vital to monitor the taxable turnover of your business, to ensure you are fully prepared when you reach the opting out limit.

The cash accounting scheme is slightly different from other VAT schemes regarding deregistration thresholds. With Cash Accounting, you do not have to leave immediately when your taxable turnover exceeds the £1.35 million joining thresholds. The scheme has a 25% tolerance built into it that allows you to continue using it until your annual taxable turnover exceeds £1,600,000.

Note: You can leave the scheme voluntarily – even without hitting the deregistration threshold.

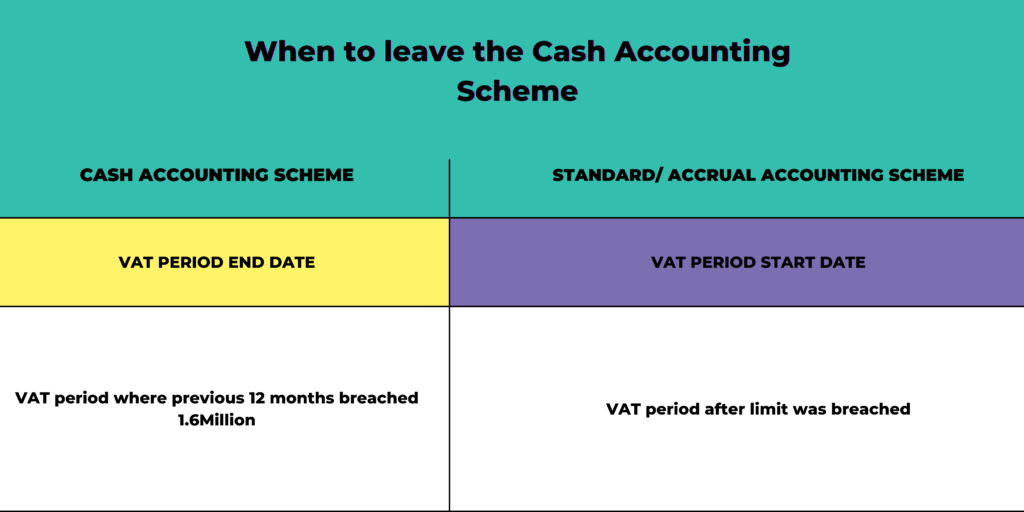

You must continually monitor the previous 12 months' taxable turnover against this £1.6million threshold. If at any point in the monthly or quarterly VAT period you breach this threshold, this period will immediately become your final period under the Cash Accounting Scheme. The next monthly or quarterly VAT period must be operated under the Standard/Accruals Accounting Scheme.

You can only opt-out of the Cash Accounting Scheme at the end of a VAT accounting period. To leave, you just start accounting for your VAT in the usual (Standard VAT) way. However, you must account for all outstanding VAT and pay HMRC any outstanding VAT when you opt out of the scheme.

Note: there’s no need to tell HMRC when you leave the scheme.

When you leave the cash accounting scheme, you must account for all outstanding VAT on supplies made and received on your final VAT return. You can either:

Read about special transactions and how to treat debts on the HMRC website. Feel free to contact us for help with your VAT support and guidance.