If you've recently relocated to or departed from the United Kingdom mid-tax year, understanding the Split Year Treatment is crucial. This unique tax provision enables individuals to strategically categorise their tax year, simplifying reporting and ensuring that only income related to the UK-resident period is taxed. In this guide, we break down the concept, clarify income reporting requirements, and provide insights on navigating the Statutory Residence Test for eligibility.

Navigating VAT requirements in Germany as a UK or non-EU Amazon seller can be complex. From understanding filing deadlines to utilizing the German VAT portal, this article simplifies the process and offers expert guidance for seamless compliance. Stay informed and ensure a successful European market expansion.

Explore the In-Depth Guide to the Winter Fuel Payment (WFP) – a vital lifeline as the UK winter approaches. Our comprehensive resource offers a deep dive into every aspect of the WFP, from eligibility criteria and payment calculations to claiming procedures. Whether you're planning for the upcoming winter season or seeking to understand the nuanced intricacies of the Winter Fuel Payment, our guide is your compass in the world of financial assistance. Stay ahead, grasp your eligibility, and maximize the full potential of this essential benefit.

Navigating the intricacies of UK VAT for Amazon FBA sellers is vital for a smooth and successful e-commerce journey. Whether you're a non-UK resident running a limited company or shipping directly to UK customers, understanding when and how Amazon collects VAT is crucial.

In this comprehensive guide, we'll break down the essentials and offer expert tips to help you stay compliant and streamline your VAT processes.

New Associated Company Rules: Time to Consider Closing Unnecessary Limited Companies With the introduction of the New Associated Company Rules by HMRC in April 2023, business owners with multiple limited companies are facing significant changes to their tax obligations. These rules are intricately linked to the recent upward adjustment in corporation tax rates, designed to impact profits exceeding £50,000 per year. As the tax rate escalates to 25% for profits over £250,000, it's crucial for business owners to comprehend the implications of these changes and consider whether closing unnecessary limited companies might be a strategic move.

Most overseas employers with employees in the UK need to operate a full PAYE scheme for their UK employees. However, if the employer can comply with the following conditions, they will not be required to operate a UK PAYE scheme, instead the UK employee will be required to operate a DPNI Scheme themselves.

Most overseas employers are subject to UK national insurance on their UK staff salaries when they have a taxable presence in the UK for PAYE purposes. If the non-UK employer has all of their UK employees working from home and does not have a physical address/office, subsidiary, branch, or taxable presence, it is likely that they will not be subject to employers' National Insurance on their UK staff wages.

Restoring a dissolved company on Companies House can seem daunting, but it's a manageable process with the right guidance. Whether you're looking to access frozen funds, recover assets, or resume operations, this comprehensive guide will walk you through the necessary steps and strategies to make your business active again. Don't let dissolution be the end of your entrepreneurial journey—take action today!

Share options are not usually taxed when they are granted, however, depending on the business issuing the share options you will be taxed at different times:

You are able to claim income tax relief upon receiving your S-EIS3 certificate from the business. The timings for the company issuing this document can be found here -

https://www.spondoo.co.uk/tips/i-have-invested-in-an-eis-or-seis-business-when-and-how-do-i-get-my-tax-relief/.

The HMRC website provides detailed instructions on how to set up a direct debit for PAYE. It is quite simple to set up a direct debit with HMRC, but it is something that the employer must do rather than agents, due to signatory on the bank account.

Businesses can defer payment of VAT on imported goods until the import procedure is completed, this is known as ‘postponed import VAT. A Postponed Import VAT Statement is an accounting document issued by HMRC and is used to declare the VAT that is due on the imported goods. Your company must be registered for the Customs Declaration Service to use Postponed VAT accounting services.

Pre-incorporation When you register for VAT, you can usually perform a pre-registration claim for your input VAT going back 6 months on services and 4 years on goods. This can prove helpful to businesses registering for VAT by providing a much needed cashflow boost. However, it can be confusing for business making this pre-registration claim when they previously trade as an unincorporated sole trader (aka self-employed business) before incorporating as a limited company.

When you buy a franchise most reasonable people would assume all your franchise fees are an obvious business expense and fully deductible. Well, HMRC's view is not quite so simple, and it requires the franchisee to treat the different elements separately. Typically franchise fees are paid as an initial lump sum, followed by a monthly or annual payment.

The Annual Accounting Scheme is a VAT scheme which allows businesses to make advance VAT payments to HM Revenue and Customs (HMRC). This can be helpful for businesses which have difficulty making VAT payments on time. If you feel that your interim payments to HMRC under the Annual Accounting Scheme are incorrect, you can request that they be reassessed by writing to HMRC. Alternatively, you can write to HMRC to ask if you can leave the VAT Annual Accounting Scheme to join another scheme.

If you are a financial advisor in the UK, you may be able to use the Value-Added-Tax (VAT) Intermediation Exemption for certain services that you provide. To qualify for the exemption, the service must be classified as "intermediation" and performed by an intermediary. Intermediation is the process of connecting two or more parties to facilitate a transaction between them. To be considered an intermediary for VAT purposes, you must be licensed by or regulated by the Financial Conduct Authority (FCA), included in the Financial Services Register (FSR), and be a member of an FCA-authorised or regulated professional body.

UK tax residents incorrectly assume that their rental income from their property in India is not reportable in their UK tax return because it is already taxable in India. If you have received Indian property rental income whilst a tax resident in the United Kingdom, this needs to be reported in your UK tax return for the relevant tax year. A foreign tax credit is then available for offset against your UK tax liability on this overseas income

If you are a tax resident in the UK and not legitimately claiming remittance basis, you need to report your worldwide income & gains. If you fail to report this in your personal tax return, the penalties vary based on whether or not you are first prompted by HMRC to make the disclosure of your overseas income.

QuickBooks allows you to customise the footer of your invoices to include your bank details. Including your bank details on your sales invoices helps your customers to set up payments easily.

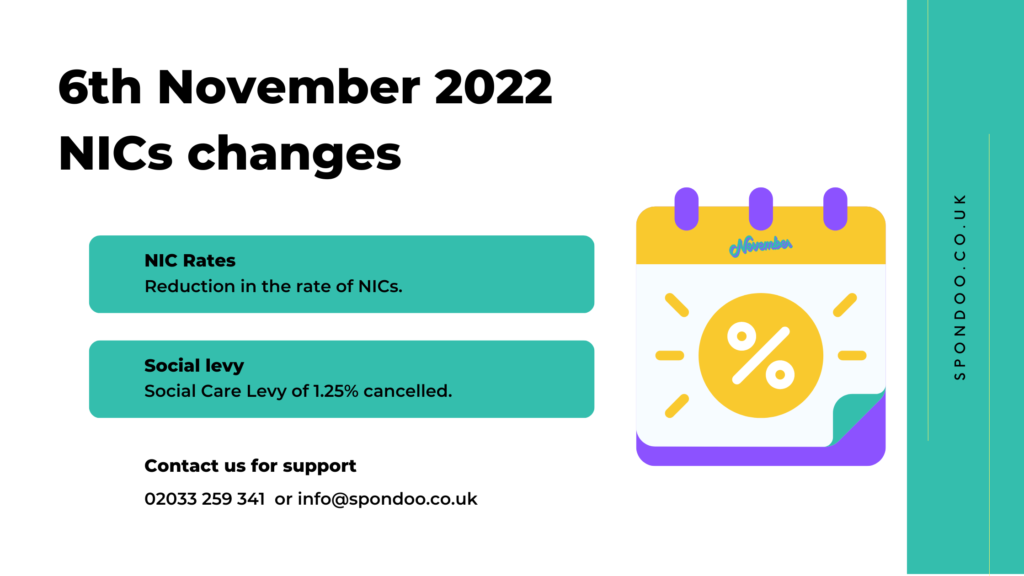

The government has Overruled the rise in National Insurance Contributions (NICs) and done away with plans for the Health and Social Care Levy. Find out the new rates NIC rates from 6th November 2022.

After submitting your VAT application there is a period where you cannot charge VAT while you wait for your VAT Number to be issued by HMRC. In this period, you have 2 options.

Your suppliers are legally bound to give you an invoice if you purchase a product or service from them. If you and your customer are VAT registered, they must provide a VAT receipt (or invoice) to make VAT claimable.

If your business is dealing with or developing land in the United Kingdom, the following points will apply: Your profits will be taxed in the UK. The Construction Industry Scheme (CIS) rules will apply.

Spondoo has a team of accountants specialising in the property industry. Our team is highly skilled with landlord tax returns and Right to Manage (RTM) obligations.

You can voluntarily backdate your VAT Registration Date for a maximum of 4 years from the date your application was received. This can be done without penalties providing you are genuinely a voluntary registration for VAT and not a mandatory registration.

HMRC view research and development for tax purposes as a straightforward project that seeks to advance/progress science or technology. When assessing if your project qualifies for the R&D tax credit, it is advisable to ensure you meet specific criteria.

Through receiving your Advanced Assurance you can give your prospective investors a reasonable degree of certainty that your business qualifies for the SEIS & EIS tax benefits.

Information provided on the site is merely guidance that may change in line with UK law and regulations. Users must not consider this to be financial advice or their sole resource when making any financial decision. Spondoo is a trading name for Accounting SQL Limited, authorised & license accounting firm under the Institute of Financial Accountants.